There is a hop in your step. And why not, you saved about 7000 bucks on a personal liability policy.

A personal what, you ask?

Well, the hallmark of an evolving society is its litigious nature. As we evolve, as a democracy, we might be slow, but we are surely becoming one. And it would be sooner rather than later that people would start having personal liability policies.

But would insurers be able to handle such volumes?

Yes, with AI, volume as well as complexity do not seem too complicated to handle.

In the ever-evolving world of risk management, liability insurance plays a crucial role in protecting individuals and businesses from financial repercussions arising from legal judgments. Whether it’s a personal injury claim due to a slip-and-fall accident or property damage caused by a mishap, liability insurance offers much-needed peace of mind.

In India, the market boasts diverse products catering to individual, professional, and corporate needs, with Public Liability Insurance (PLI) and Product Liability Insurance (PLI) being the most prevalent. However, the industry is now witnessing a paradigm shift with the introduction of Artificial Intelligence (AI), promising a future of increased efficiency, personalized risk assessment, and proactive claims management. Let’s delve into how AI is and can possibly revolutionise liability insurance beyond recognition.

What’s on this page?

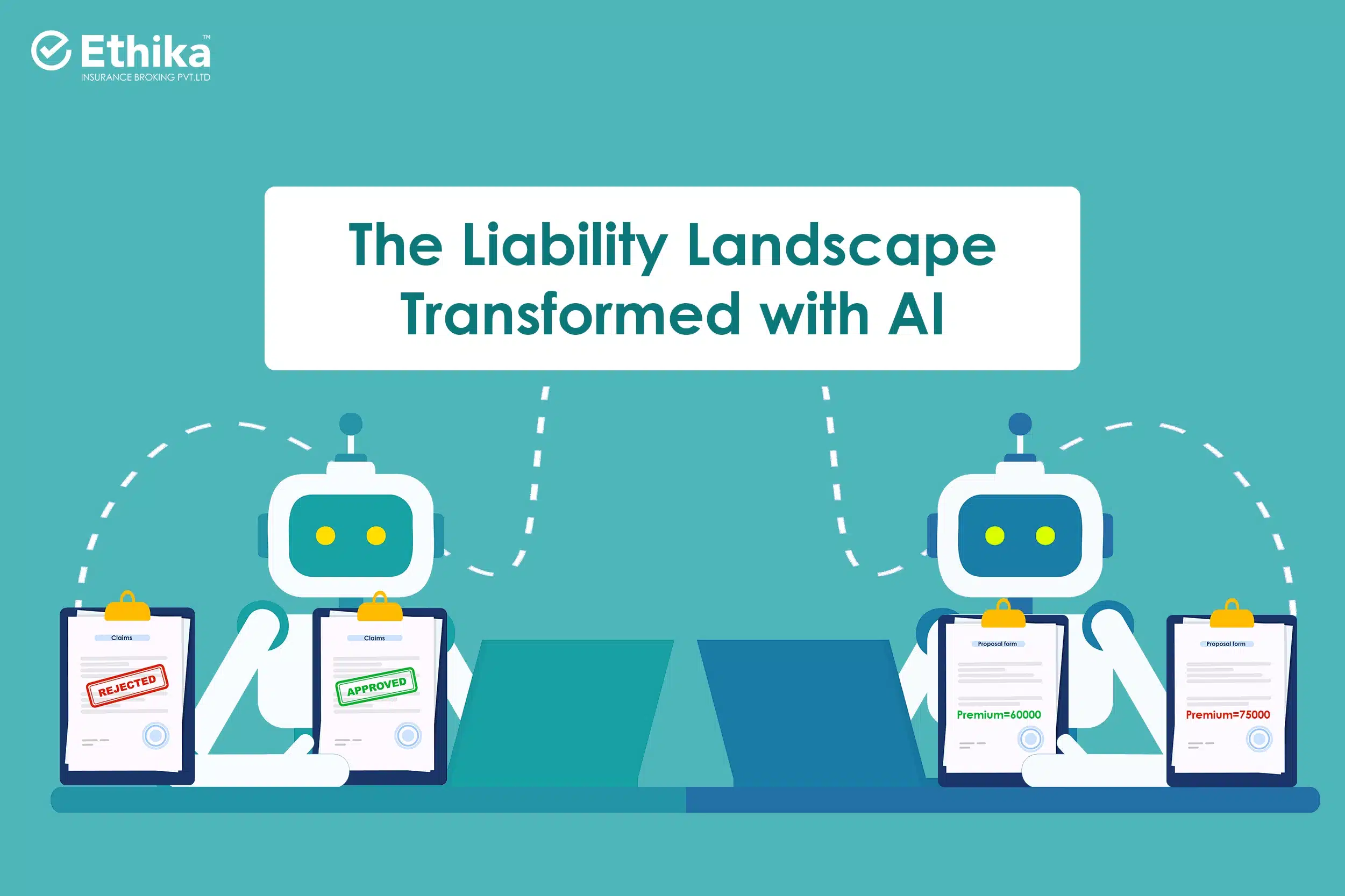

From Manual Work to Algorithmic Accuracy: Fraud Detection Redefined

Fraud poses a significant challenge to insurers, impacting premiums and claim payouts. Traditionally, detecting fraudulent claims relied heavily on manual investigations, a time-consuming and error-prone process. Enter AI, the game-changer with its advanced data analysis and machine learning capabilities. Imagine insurers analyzing vast datasets of claims history, identifying suspicious patterns or inconsistencies in medical records. AI algorithms can flag potentially fraudulent claims with remarkable accuracy, saving costs and ensuring genuine policyholders receive timely settlements.

Personalized Premiums and Risk Assessment: Beyond Blanket Solutions

Traditionally, liability insurance premiums were largely determined by broad risk categories, often leading to unfair pricing for low-risk individuals or businesses. AI empowers insurers to break free from this limitation. Imagine utilizing historical data on accident rates, safety practices, and claim trends within specific professions or industries. AI models can then generate personalized risk profiles, leading to tailored premiums that accurately reflect individual risks. This not only benefits low-risk policyholders with lower premiums but also allows insurers to offer more competitive pricing strategies.

From Reactive Claims Management to Proactive Risk Mitigation

Liability insurance traditionally focused on claims settlements after incidents occurred. AI, however, opens doors to a proactive approach. Imagine sensors and devices equipped with AI capabilities being integrated into workplaces or personal environments. These systems can monitor safety protocols, identify potential hazards, and even predict accidents in real-time. AI can then alert individuals or businesses to take corrective actions, preventing accidents and minimizing potential liability claims.

Challenges and the Road Ahead: Embracing the Future

While AI boasts immense potential, challenges remain. Data privacy concerns need to be addressed, and ensuring responsible AI development is crucial. However, the industry is actively tackling these challenges. Regulatory frameworks are being established, and ethical considerations are being incorporated into AI development processes. As technology matures and costs decrease, AI is poised to become a mainstream tool, transforming the liability insurance landscape in India.

The future of liability insurance in India is brimming with possibilities thanks to AI. With personalized risk assessments, efficient claims management, and proactive hazard mitigation, AI promises a future where individuals and businesses are better protected and empowered to manage their liability risks effectively. This will not only benefit policyholders and insurers but also contribute to a safer and more secure society for all.

How can AI prevent fraud in liability insurance?

AI analyzes vast datasets of claims history, identifying suspicious patterns or inconsistencies in details, medical records, or repair estimates, flagging potentially fraudulent claims with remarkable accuracy. This helps insurers save costs and ensures genuine policyholders receive timely settlements.

How can AI personalize liability insurance premiums?

AI analyzes historical data on accidents, claims trends, and safety compliance within specific professions or industries. This helps generate personalized risk profiles, leading to tailored premiums that accurately reflect individual exposures. Low-risk policyholders benefit from lower premiums, while insurers offer competitive pricing.

Can AI prevent accidents and reduce liability claims?

Yes! AI-powered sensors and wearables integrated into workplaces or personal vehicles can monitor safety protocols, identify hazards, and even predict accidents. This allows individuals and businesses to take corrective actions proactively, minimizing potential liability claims.

What other types of liability insurance can benefit from AI?

Beyond PLI and PLI, AI can analyze online reviews for cyber risks, utilize historical data for personalized Directors & Officers premiums, and personalize professional indemnity insurance for doctors based on their individual risk profiles.

What are the challenges of using AI in liability insurance?

Data privacy concerns and responsible AI development are key challenges. However, the industry is actively addressing these issues through regulatory frameworks and ethical considerations in AI development processes.