We added the most missing element

in Employee Group Health Insurance,

Employee Happiness

Book 15 minutes call with us and we will surprise you

Book 15 minutes call with us and we will surprise you

In our opinion, the real purpose of employee health insurance should not be

limited to providing financial assistance to employees when they become sick,

But to prevent them from getting sick in the first place.

To keep them healthy,

To make them happier.

No its Not Employee Satisfaction

No its Not Talent Acquisition

No its Not Better Salaries

No its Not Performance Management

You guessed it right

And We have already seen the future has arrived,

faster than we anticipated, because of the pandemic.

We are an Insurance Broking Company that understands the value of employee happiness

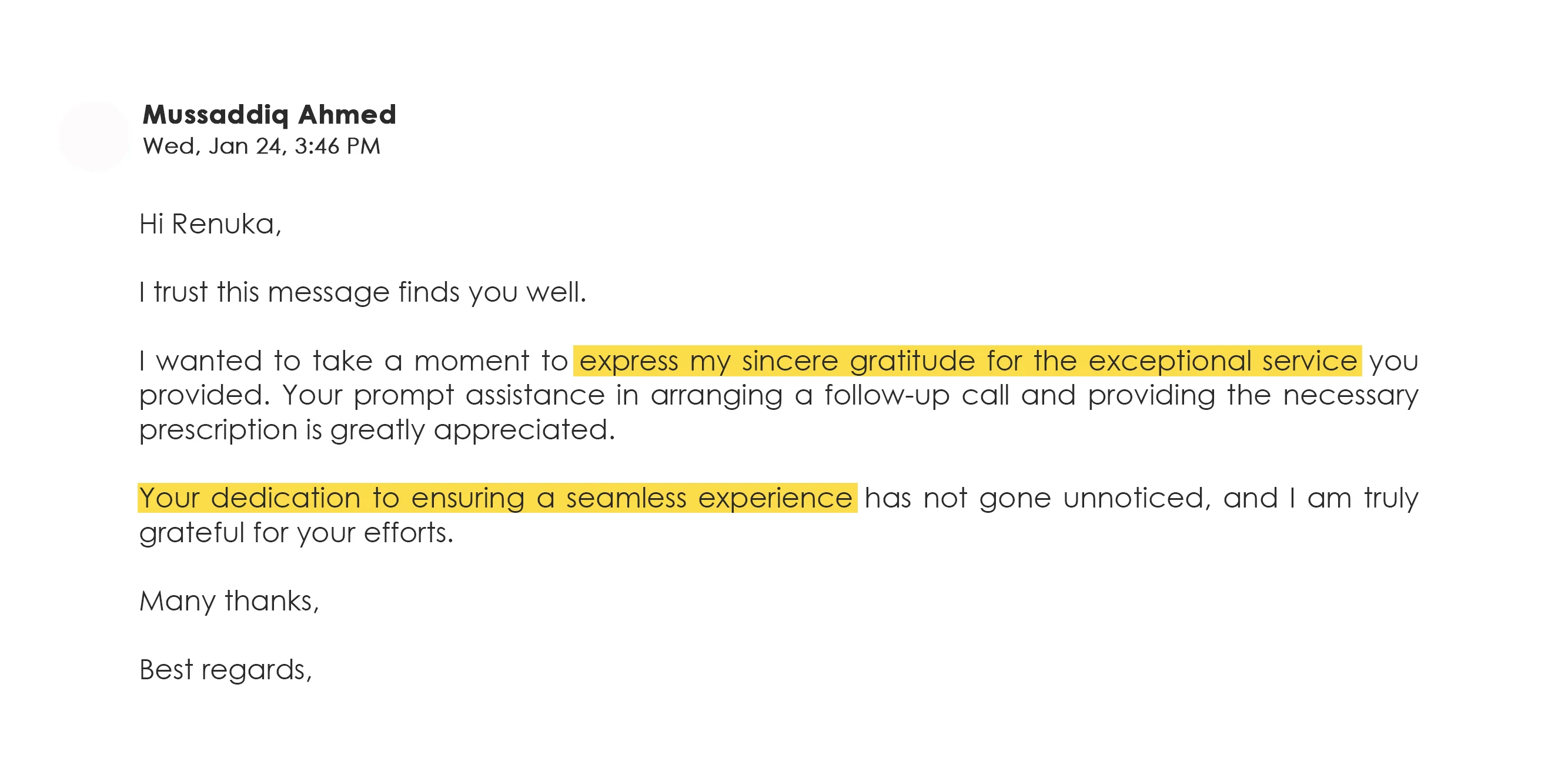

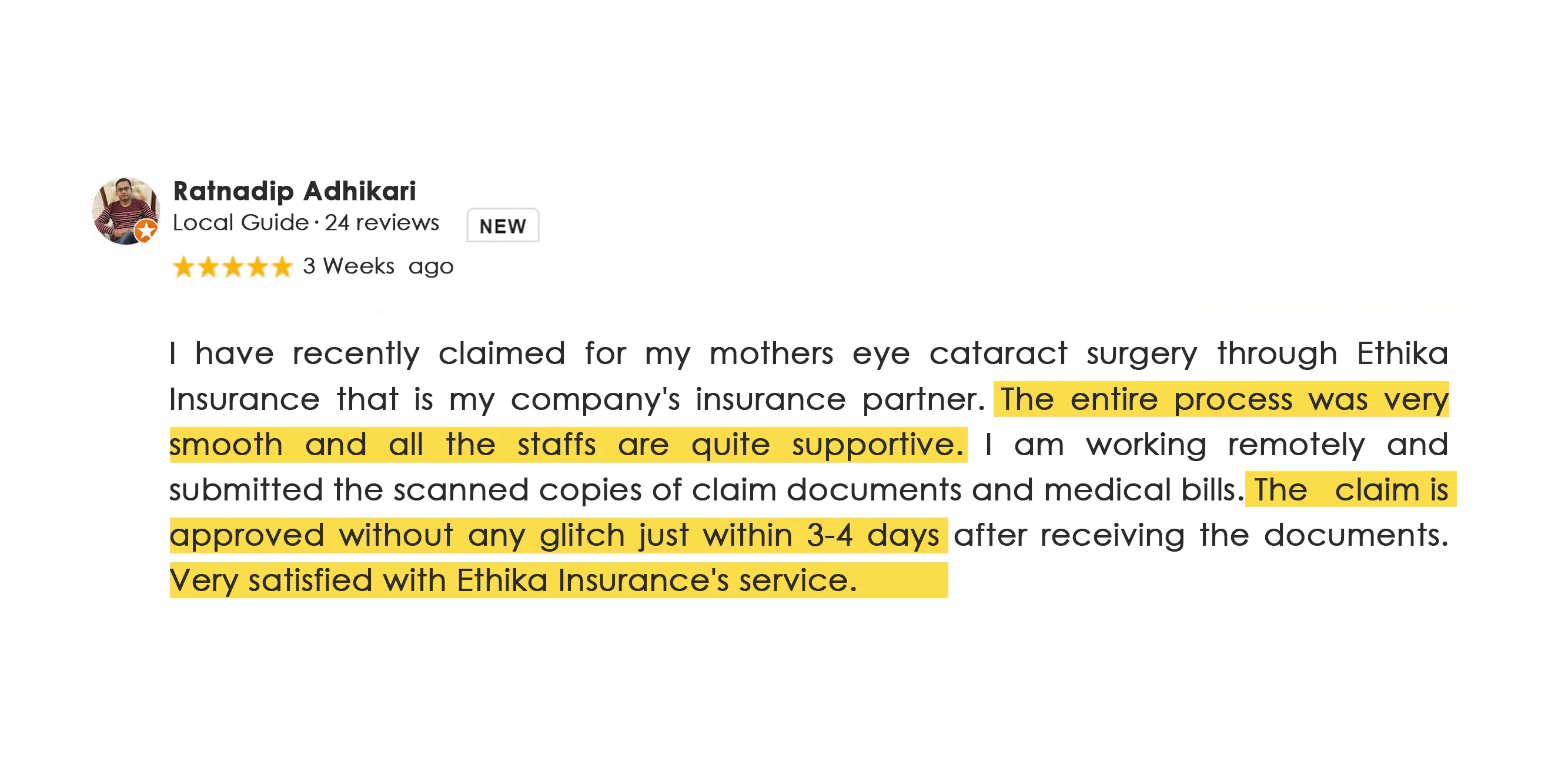

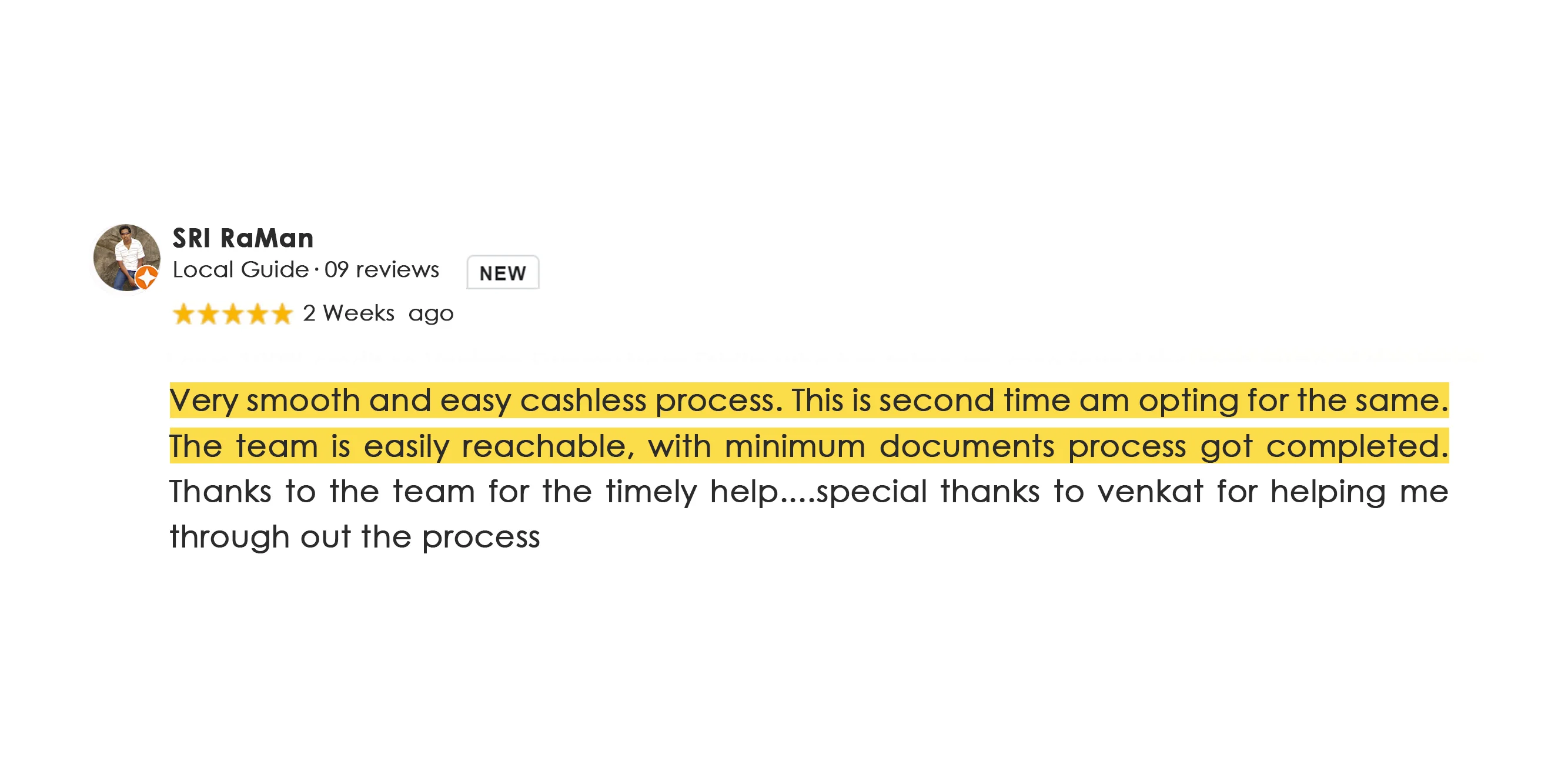

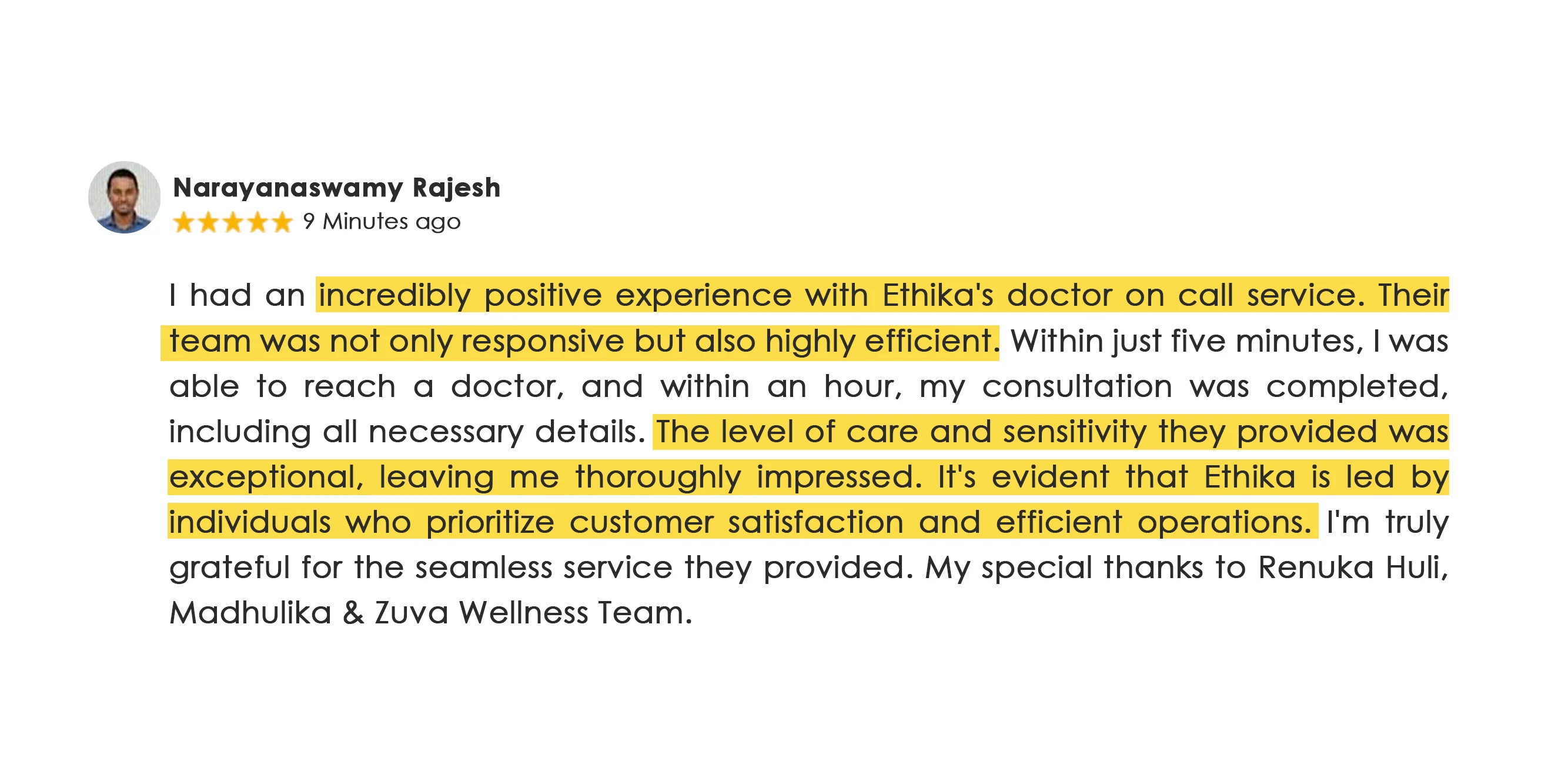

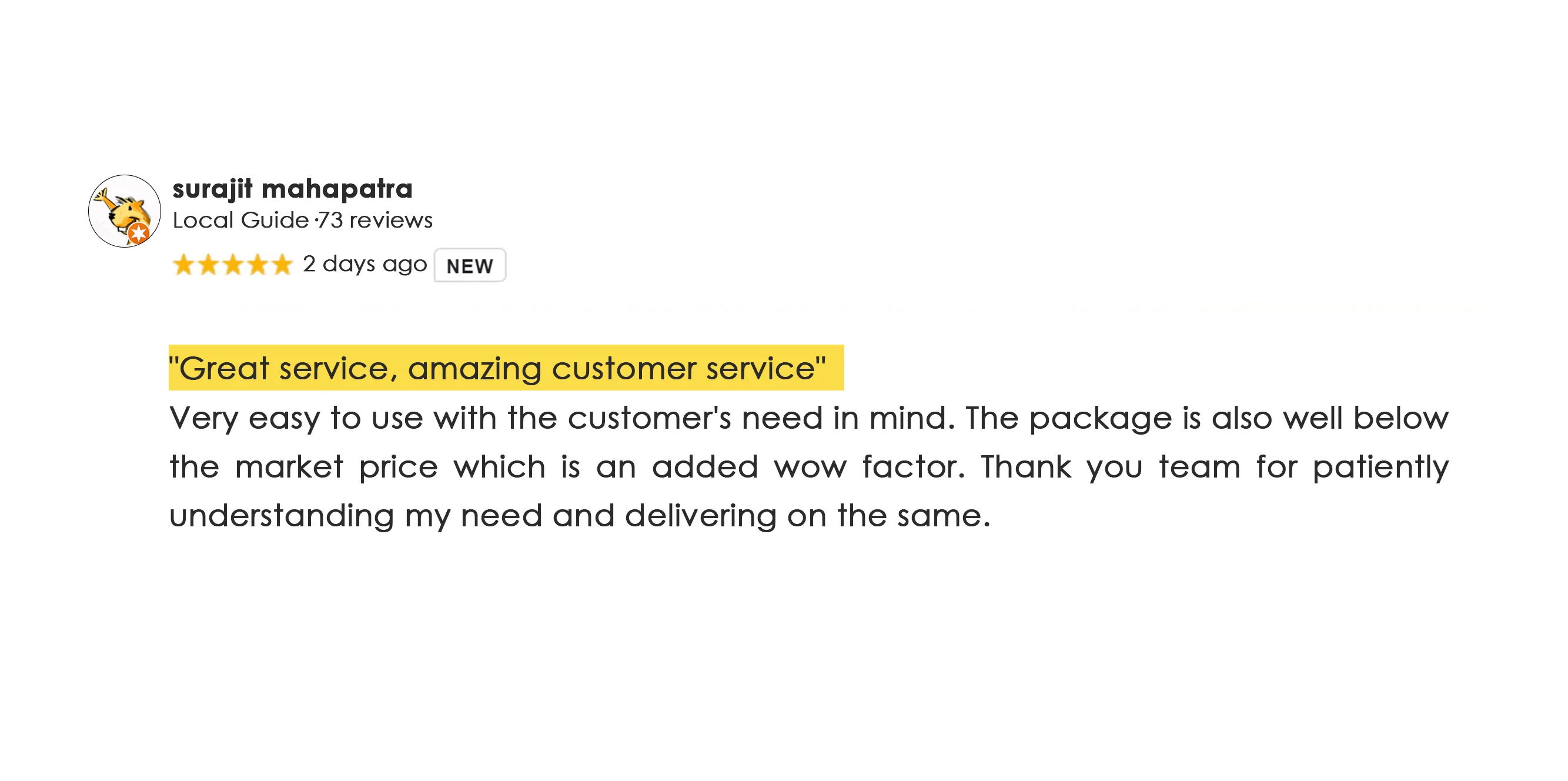

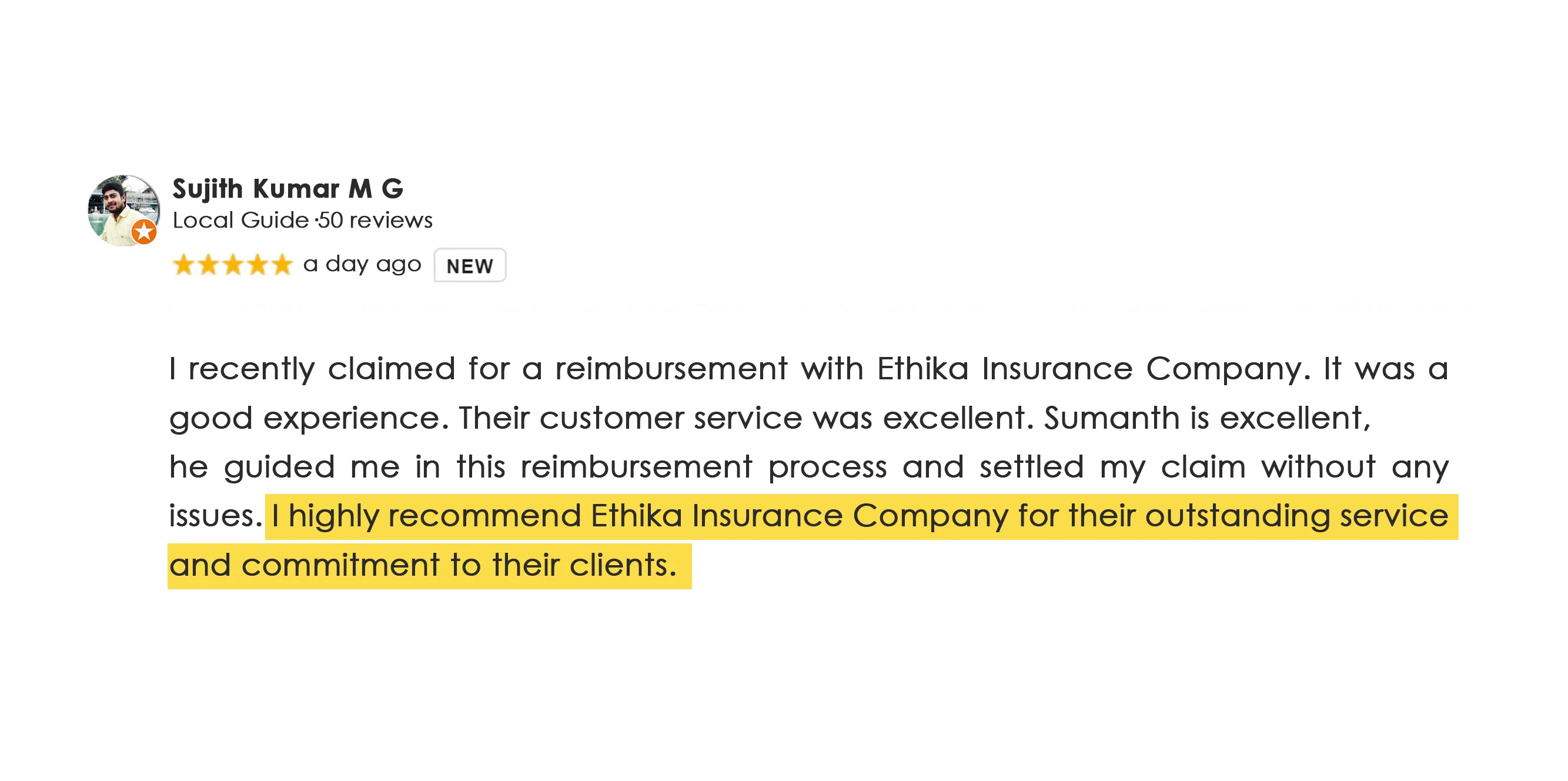

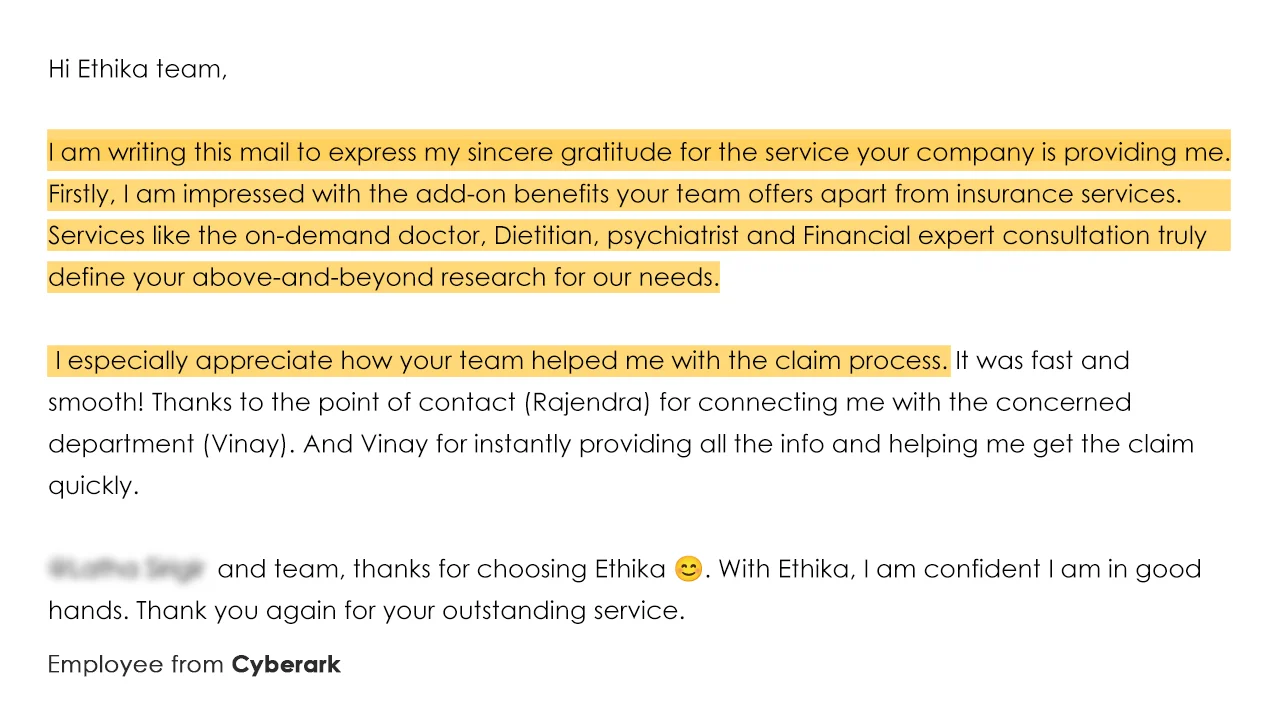

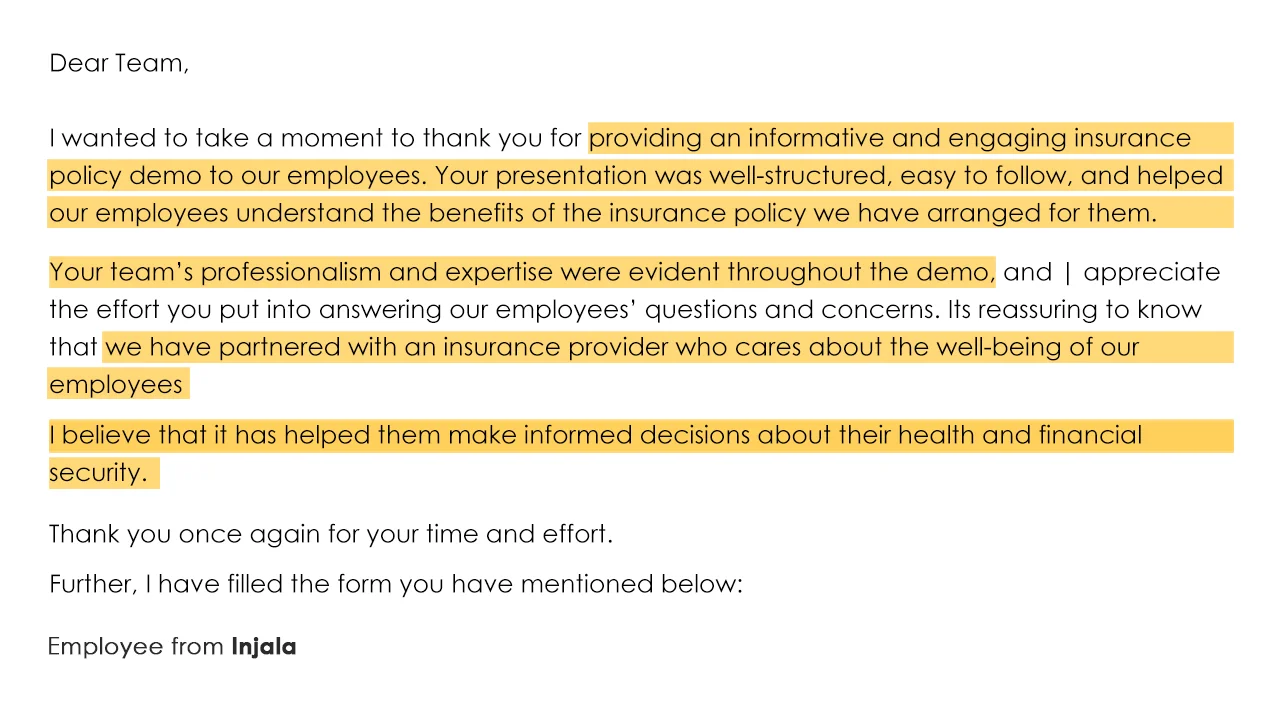

Get every Health Insurance Claim settled fast along with applause from your employees.

Your employees can be more productive by teaching them how to be happier rather than avoiding unhappiness.

Spend not more than 5 Min in managing your group insurance and other employee benefits.

Group OPD Expenses Insurance

Upgrade their Health Insurance cover

at just 500 for 50 lacs

Life Insurance Top up

Errors and Omissions Liability Insurance