The average medical cover provided by an employer is generally in the range of Rs 3 Lakh to Rs 5 Lakh, however considering the medical expenses in current medical settings, do you think that the coverage by the employer is enough?

Yes

No because:

It covers higher value of claims and surprisingly very low cost of premiums. It does not cover the lower value of claims and that can be covered from your pocket or from your employer group health insurance or from any other regular health insurance policy.

In-fact it is a wise idea to first cover ourselves with a higher amount of claims through Super top up Insurance and then if our budget permits, we can cover for a lower amount of claims too

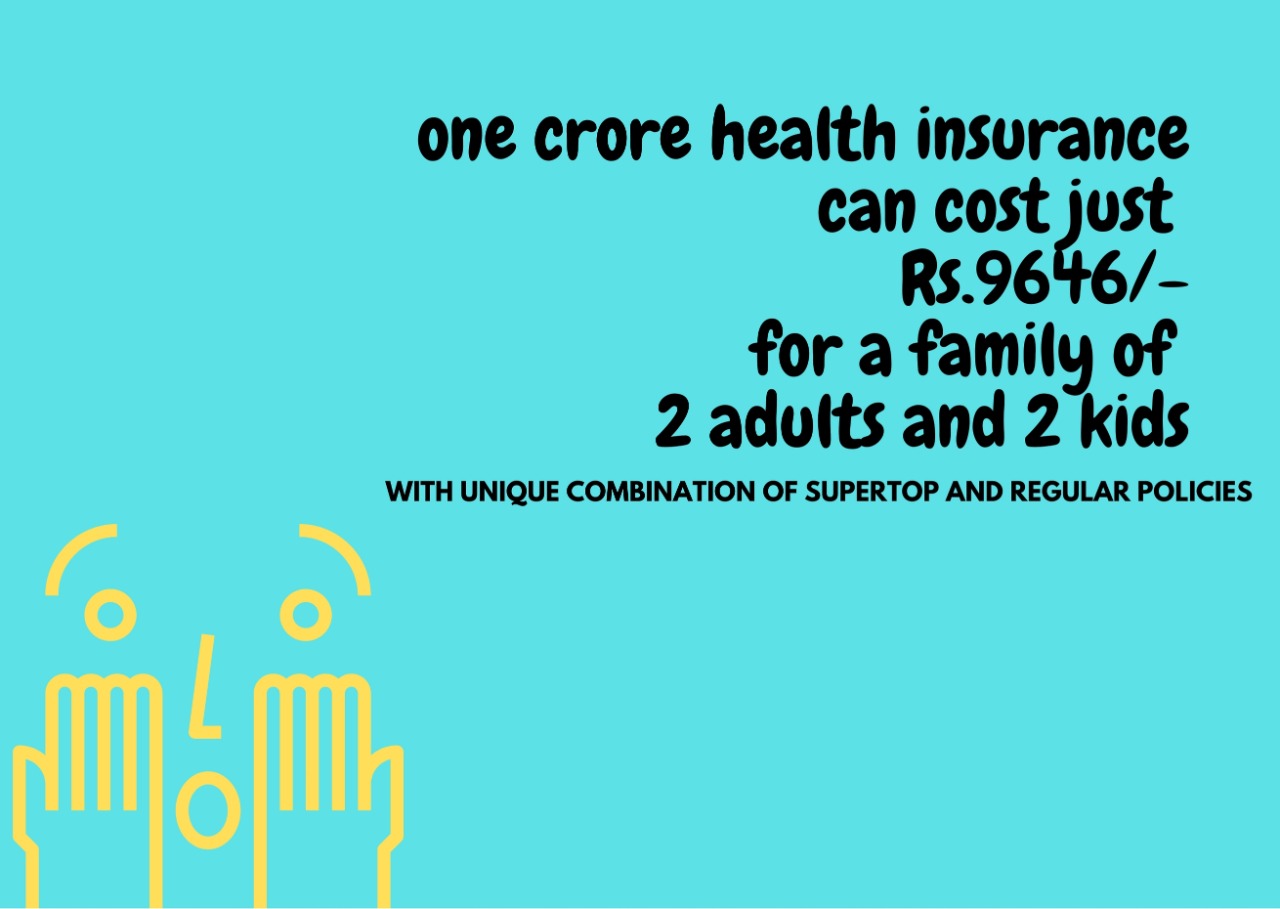

A 1 crore health insurance plan for 30 years person will cost just Rs.687 per year with deductible of 10 lacs.

Let’s understand how super top up works

Mr. Raju had a major Surgery for which the medical expenses were Rs 9 lakhs. His insurance policy provided by his company had a threshold limit of Rs 3 lakhs. When his boss asked how he would manage the rest of the expenses, Mr. Raju said that he has a Super top-up plan.

A regular health insurance policy has a sum insured limit, beyond which it does not cover any expenses. This is when a Super top-up policy is useful, it becomes effective soon as the sum assured from a health plan is exhausted. Therefore, Ms.Raju can claim the balance amount of Rs 6 lakhs from his super top-up health cover. So essentially, he has a super top up plan with a deductible of Rs 3 lakhs.

Let’s say you have taken two policies

Case 1: If the claim is of 9 lacs

Policy 1: will pay 3 lacs which is equal to its sum insured. If you don’t have a base policy or corporate policy, then this amount will be paid from your pocket.

Policy 2: This policy will pay above 3 lacs (which is deductible). That means 6 lacs (9-3=6) will be paid from this policy. You will be still having a balance sum insured of 4 lacs (10 lacs – 6 lacs = 4 lacs) in the super top up policy which can be utilised in any future claims.

DON’T GET CONFUSED BETWEEN TOP UP AND SUPER TOP UP :

A super top up comes to the rescue when a single claim does not cross the deductible limit of top up policy, but multiple claims do. Thus, if Mr.Raju submitted three different claims of Rs 3 lakhs, Rs 3 lakhs and Rs.3 lacs respectively, the top up plan would be useless since none of them exceed Rs 3 lakhs individually.

But in Super top up, all the three claims will be added up the total claim beyond 3 lacs deductible, which in this case will be 6 lacs is payable.

Thus one should always choose Super top up instead of Top up.

Like any other health insurance policy it covers the inpatient hospitalization expenses incurred due to an illness or accident, for a minimum of 24 hours. It pays for medical expenses including room rent, nursing, medical practitioner, boarding expenses, ICU, Operation theatre, medicines and other related requirements.

With the advancement in medical technology, in certain surgeries, the inpatient Hospitalisation can be of less than 24 hours. Those are called day care procedures. Insurer keeps identifying those procedures and settles the claim and waives that 24 hours minimum hospitalisation clause. It is advisable to refer cases to the Insurer and take prior approval before hospitalisation.

It also Covers outpatient medical expenses such as Doctor Consultations, diagnostic tests, medicines etc. that occur during the specified number of days immediately before and after hospitalization.

The Pre-Existing Diseases are not covered under the policy for a certain period (known as a waiting period) as mentioned in the policy. Waiting period starts from the date of inception of first policy with the insurer. Under this period the policy should have continuous coverage and should not have any break.

It is necessary and in the interest of the Policyholder to declare all the known pre-existing diseases one is already having. The insurer may reject the claim if they find that the policyholder has intentionally not declared the existing disease at the time of first taking the policy even when the claim is made after the Pre-existing waiting period.

A loading on your premium amount may be applicable as per nature of such pre-existing disease. Not all pre-existing diseases will attract loading. Applicability & percentage of loading will be ascertained by a medical underwriter. If loading is applicable for your health insurance proposal, the insurer will send you a counter offer. Only if you accept this offer and pay an additional premium, the insurer will issue the policy. If you do not accept such a counter offer within 15 days, the policy will not be issued, and the premium will be refunded after adjusting for expenses incurred by us on your pre-policy medical check-up.

There is no claim-based loading. However, if there was a loading based on the customer’s health condition on policy premium at the time of the first issuance of this policy, the same loading will be applicable at the time of renewal as well.

You are eligible for a deduction of INR 25000 for a premium paid on the health for yourself, for your spouse and children. Also, if you pay the health insurance premium for your parents (Senior Citizen), you will be entitled to an additional deduction of Rs. 30000/- Tax benefit is applicable if the premium is paid by any mode of payment, other than cash

Good news is that the premium will not change and neither the insurer can refuse to renew the policy, irrespective of the claims in previous year policy.

Your policy premium can change in case of following conditions:

Is there any advantage of buying this policy from an Insurance Broker?

You can buy from Broker, Agent, Directly from the Insurance company office or from their website or Online from a web aggregator website.

An Insurance broker is bound by the Insurance Regulator to perform as per the terms laid to them. They need to protect the interest of the client (you) at every step of insurance, be it buying or claiming assistance and representing the clients to the Insurer and not the other way around. That is why they are the only legal entity which is not tied with any particular Insurance company. They can deal with any Insurance company.

Now, because they are experienced and have worked with various clients, they know the best practices and hence can help you set up the best insurance policy for your organisation with ease, saving your time and effort.

Check the most suitable super top up plan with your choice of deductible here at www.ethika.co.in

Check our testimonials of our insured who claimed here.

Reach us through whats up @ 6304901240